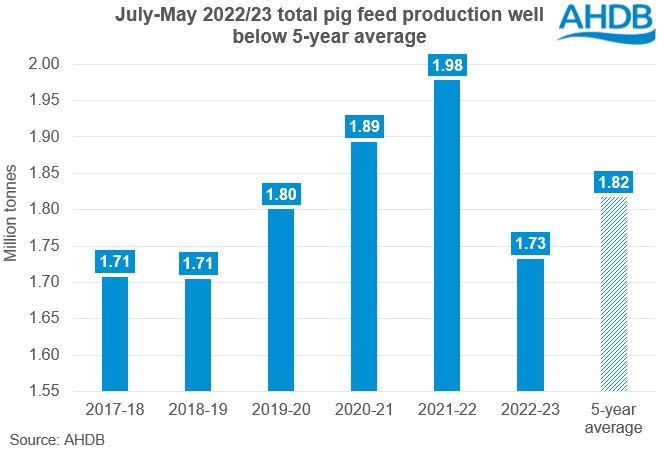

As was documented over the last marketing year, the 2022/23 season saw reductions in cereals usage for animal feed. Pig and poultry feed demand saw the biggest declines in percentage terms, with total pig feed production from July to May down 12.4% when compared with the same period the previous year.

Based on 5-year averages (2017/18 – 2021/22), pig feed production accounts for c.17% of total animal feed production, so it’s important to consider what might happen to herd numbers going forward, as this will impact domestic cereals usage.

According to recent analysis, the UK pork marketplace remains very tight with year-to-date production and slaughter figures for the first half of the year recording significant year-on-year declines. From January to June this year, UK pig meat production totalled 457.1 Kt, the lowest volume for that period in 6 years.

However, on Monday, AHDB published the latest quarterly pork cost of production and margin estimates for 2023 Q2. These estimates show improvements in cost of production and net margins, which have not been seen since 2020 (see more information below).

Anecdotal reports generally suggest that a gradual recovery can be expected in the pig herd, and that there is cautious optimism in the sector. In the June pork market outlook, breeding herd numbers are still expected to increase by 7,000 head between June 2022 and June 2023.

If we do in fact see this gradual rebound in the pig herd, we could see feed demand begin to pick up and these recent declines in feed to shrink over the next few months. Though it is unlikely we will see pig feed production increase back to 2021/22 levels anytime soon.

Credit: Source link